If you are a partner in a business partnership or a member of a multi-member LLC, there is one tax document you need to understand before anything else. It is not the return the partnership files with the IRS. It is the document the partnership prepares for you personally. It is called a Schedule K-1, and it is what determines what you report on your own federal income tax return every year.

Here is a clear, practical explanation of what a K-1 is, where it comes from, what it contains, and what you are expected to do with it.

A Schedule K-1 is a tax form that a partnership issues to each of its partners at the end of every tax year. It reports each partner's individual share of the partnership's income, losses, deductions, credits, and other tax items for the year. Think of it as the partnership's way of telling you (and the IRS) exactly how much of the business's financial activity belongs to you.

The K-1 comes directly out of the partnership's Form 1065, the US Return of Partnership Income. When the 1065 tax return is prepared, the total income and deductions are allocated across all partners on Schedule K. From that summary, a separate K-1 is generated for each individual partner. If the 1065 partnership return is inaccurate, every K-1 that flows from it is inaccurate, and every personal return that depends on those K-1s is affected downstream.

The partnership itself does not pay federal income tax. Instead, all of the business's tax items pass through directly to the partners. This is what it means to be a pass-through entity, and the K-1 is the mechanism that makes that pass-through happen.

Your K-1 will reflect your distributive share of whatever the partnership earned or lost during the year. That share is determined either by your ownership percentage or by the specific terms of your partnership agreement. The agreement governs how income, losses, and other items are split, which is why having a clear, well-drafted partnership agreement is important long before 1065 tax preparation begins.

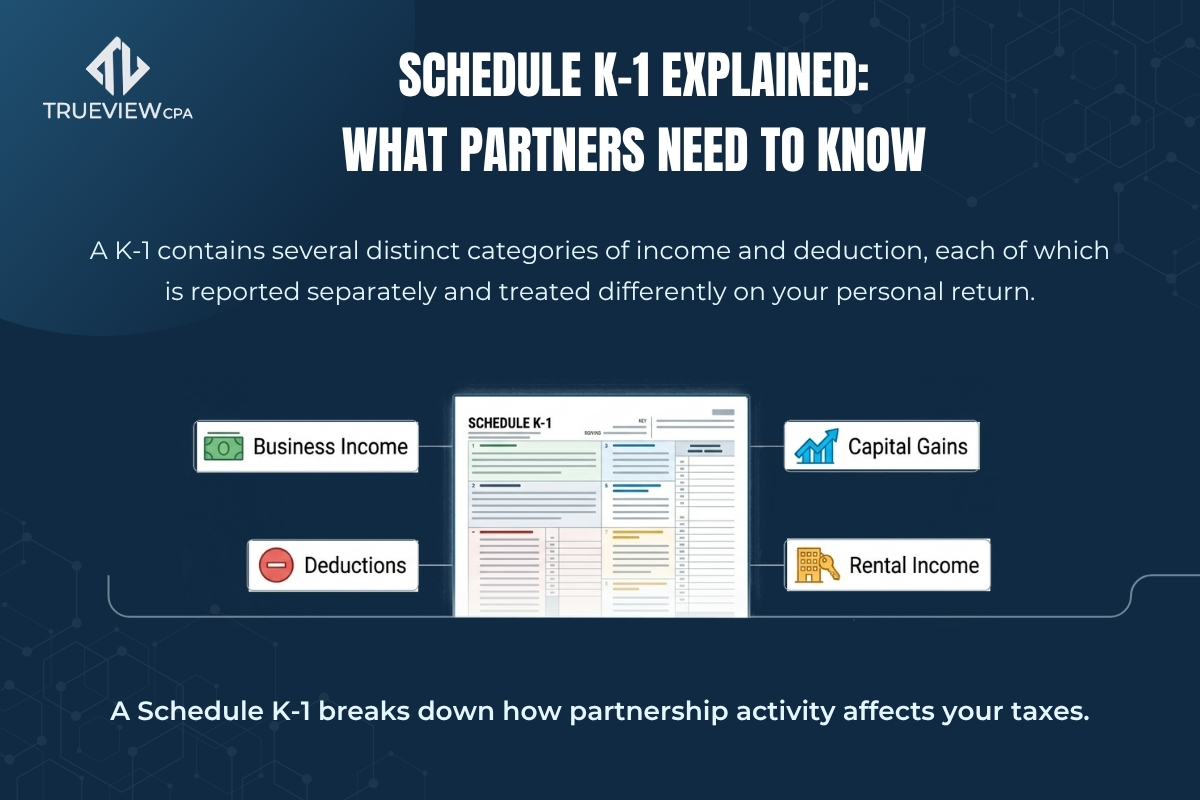

A K-1 contains several distinct categories of income and deduction, each of which is reported separately and treated differently on your personal return. The most common items you will see include ordinary business income or loss, which is your share of the partnership's net profit or loss from its regular operations. You may also see rental income or loss if the partnership holds real estate, interest income, dividends, capital gains or losses from asset sales, and Section 179 deductions or other depreciation-related items.

Guaranteed payments are another item that appears on many K-1s. These are payments the partnership makes to a partner for services or for the use of capital, regardless of whether the partnership was profitable. Guaranteed payments are treated as ordinary income and are generally subject to self-employment tax, even for partners who might otherwise be exempt.

Each of these items carries its own tax treatment and feeds into different parts of your personal return. This is one of the reasons 1065 tax prep at the entity level requires precision. A misclassified item on the 1065 does not just affect the partnership. It affects every partner's return in a different way depending on their individual tax situation.

One of the most important things to understand about K-1 income is that your tax obligation is based on your distributive share of partnership income, not on what was actually distributed to you. If the partnership earned $400,000 for the year and your share is 30 percent, you report $120,000 of income on your personal return. It does not matter whether the partnership paid you anything at all.

This creates a real cash flow challenge for partners in profitable businesses that reinvest their earnings. You owe income tax on money you may not have received, and because no employer is withholding taxes on partnership distributions, you are responsible for making quarterly estimated payments throughout the year. Failing to do so results in underpayment penalties in addition to the balance owed at filing.

The 1065 filing deadline is March 15, which is one month before the individual return deadline of April 15. Partnerships that file on time should have K-1s out to partners around that same period. However, many partnerships file extensions using Form 7004, which pushes the partnership deadline to September 15. If your partnership files an extension, your K-1 may not arrive until late summer or early fall, which means you will likely need to extend your own personal return as well.

This timing dependency is worth understanding early in the year, particularly if you are planning around an April filing. The K-1 is not optional information you can work around. It is required to complete your personal return accurately.

If you are a general partner, your share of ordinary business income reported on your K-1 is generally subject to self-employment tax in addition to regular income tax. For 2025, that is 15.3 percent on net earnings up to the Social Security wage base and 2.9 percent on everything above that threshold.

Limited partners are generally not subject to self-employment tax on their distributive share of income, though guaranteed payments remain taxable regardless of partner classification. Members of a multi-member LLC that files a Form 1065 follow the same rules, which is why understanding your role in the partnership structure matters when estimating what you will owe.

Receiving a K-1 is not the end of the process. Each item on the form needs to be entered correctly on your personal return, and the tax treatment of each line is not always straightforward. Passive activity rules, at-risk limitations, and basis restrictions can all affect whether a loss reported on your K-1 is actually deductible in the current year. A professional 1065 tax preparer working on the partnership return and a CPA handling your personal return need to be coordinated, or errors compound quickly.

1065 tax services that include both the entity-level return and K-1 preparation ensure that every partner receives accurate information they can hand directly to their own advisor. 1065 filing services that extend through the filing season give partners the support they need to respond to questions and file complete, accurate personal returns without delays.

At TrueView CPA, partnership tax return preparation and 1065 tax preparation for partnerships are core parts of our practice. If you have questions about a K-1 you received, need help understanding what it means for your personal return, or want a CPA for your 1065 tax return who will handle both the entity and the partners correctly, we are happy to start with a conversation.

Need help understanding your Schedule K-1 or partnership tax obligations? Schedule a call with our tax professionals today for clear, reliable guidance tailored to your situation.

.svg)