When two or more people go into business together, the entity structure question comes up quickly. Should you form an LLC or operate as a partnership? And once you have made that decision, how does it actually affect what you file with the IRS each year?

The honest answer is that the distinction between LLCs and partnerships is more nuanced than most people expect, particularly when it comes to taxes. Here is a clear breakdown of how each structure works, where they overlap, and what the tax differences actually mean in practice.

A partnership is a business arrangement between two or more people who share ownership, profits, and losses. It does not require formal registration with a state in most cases. It exists by default when two or more people carry on a business together with the intent to make a profit.

An LLC, or limited liability company, is a legal entity created by filing articles of organization with a state. It provides limited liability protection to its members, meaning personal assets are generally shielded from business debts and liabilities. A partnership does not provide this protection by default for general partners.

This liability distinction matters significantly for legal purposes. For tax purposes, the picture is more complicated because the IRS does not have a separate tax category called an LLC. Instead, it taxes LLCs based on how many owners they have and whether they have made any elections.

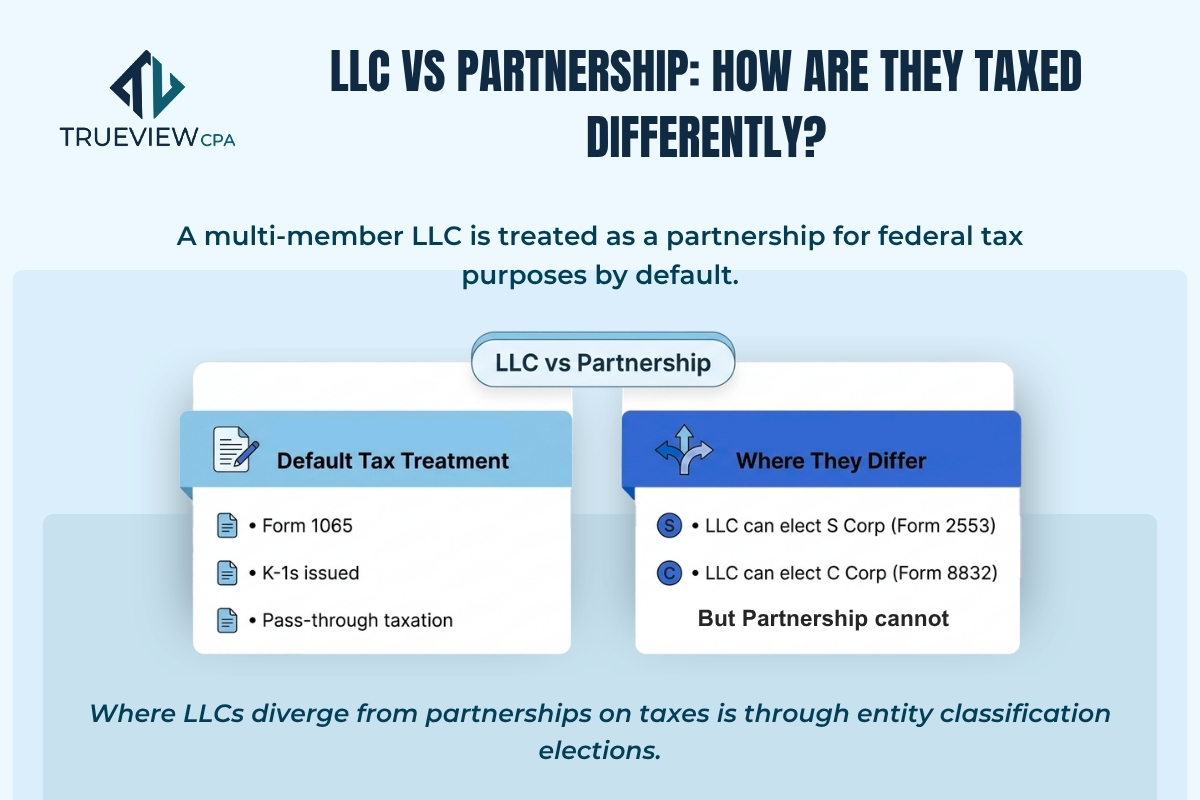

A multi-member LLC is treated as a partnership for federal tax purposes by default. That means it files a 1065 partnership return, prepares Schedule K-1s for each member, and passes income and losses through to the members' individual returns.

From a tax standpoint, a default multi-member LLC and a general partnership are treated almost identically by the IRS. Both file Form 1065. Both issue K-1s. Both use pass-through taxation. The legal liability protection differs significantly, but the federal tax treatment does not.

This surprises a lot of LLC owners who assumed their entity structure meant a different kind of tax filing. If you formed a two-person LLC without making any tax elections, you are filing a partnership tax return whether you knew it or not.

Where LLCs diverge from partnerships on taxes is through entity classification elections. An LLC can elect to be taxed as an S corporation by filing Form 2553 or as a C corporation by filing Form 8832. A general partnership cannot make these elections because it is not a separately organized legal entity.

When an LLC elects S corp status, it files Form 1120-S instead of a 1065. The income still passes through to members, but the tax treatment of owner compensation changes significantly. Owner-operators pay themselves a reasonable salary as W-2 employees and take additional income as distributions, which are not subject to self-employment tax. For members with meaningful net income, this can produce real tax savings.

When an LLC elects C corp status, it files Form 1120 and pays corporate income tax at the entity level. Profits distributed to members as dividends are then taxed again at the individual level. This double taxation makes the C corp election less attractive for most small businesses, though it can make sense in specific circumstances involving retained earnings or venture capital investment.

For members of a multi-member LLC taxed as a partnership and for general partners, all ordinary business income is generally subject to self-employment tax in addition to income tax. For 2025, self-employment tax is 15.3% on net earnings up to the Social Security wage base and 2.9% on everything above that.

This is one of the primary reasons business owners consider the S corp election once their net income reaches a level where the self-employment tax savings outweigh the additional compliance costs of running payroll and filing a separate corporate return.

Limited partners in a limited partnership have historically been exempt from self-employment tax on their distributive share of partnership income, though this area of law has nuance and the IRS has challenged certain arrangements that attempt to characterize what are effectively active business earnings as limited partner income.

Federal tax treatment is only part of the picture. Many states impose their own taxes on LLCs that do not apply to general partnerships. California, for example, charges an annual LLC fee based on gross receipts in addition to the state minimum franchise tax. Texas imposes a franchise tax on LLCs but not on general partnerships below certain thresholds.

If you are operating in a state with significant LLC-specific taxes, the entity structure choice has tax implications beyond the federal return that are worth evaluating with a professional before you file.

If your business is a general partnership or a multi-member LLC that has not made a tax election, you are filing a 1065 tax return and preparing K-1s for each owner. The mechanics are the same regardless of whether your state-registered entity is called a partnership or an LLC.

Partnership tax preparation for both structures involves the same core elements: accurate income and expense reporting, correct allocation of income among partners or members, capital account maintenance, and timely K-1 preparation so every owner can file their own return on time.

At TrueView CPA, we handle 1065 partnership filing for both traditional partnerships and multi-member LLCs, including situations where members are evaluating whether an S corp election might make sense going forward. If you want to understand how your current structure affects what you owe, we are happy to take a look.

Not sure whether an LLC or Partnership is right for your business? Schedule a call with our experts today and get personalized guidance on choosing the most tax-efficient structure for your needs.

.svg)