If you recently formed a partnership or brought a business partner into your existing operation, one of the first tax questions that tends to come up is whether the business itself owes federal income tax. It is a fair question, and the answer often surprises people who are new to running a business with someone else.

The short answer is no. A partnership does not pay federal income tax at the entity level. But that does not mean the income goes untaxed. Here is a clear explanation of how partnership tax actually works, what it means for each partner, and why getting the filing right matters.

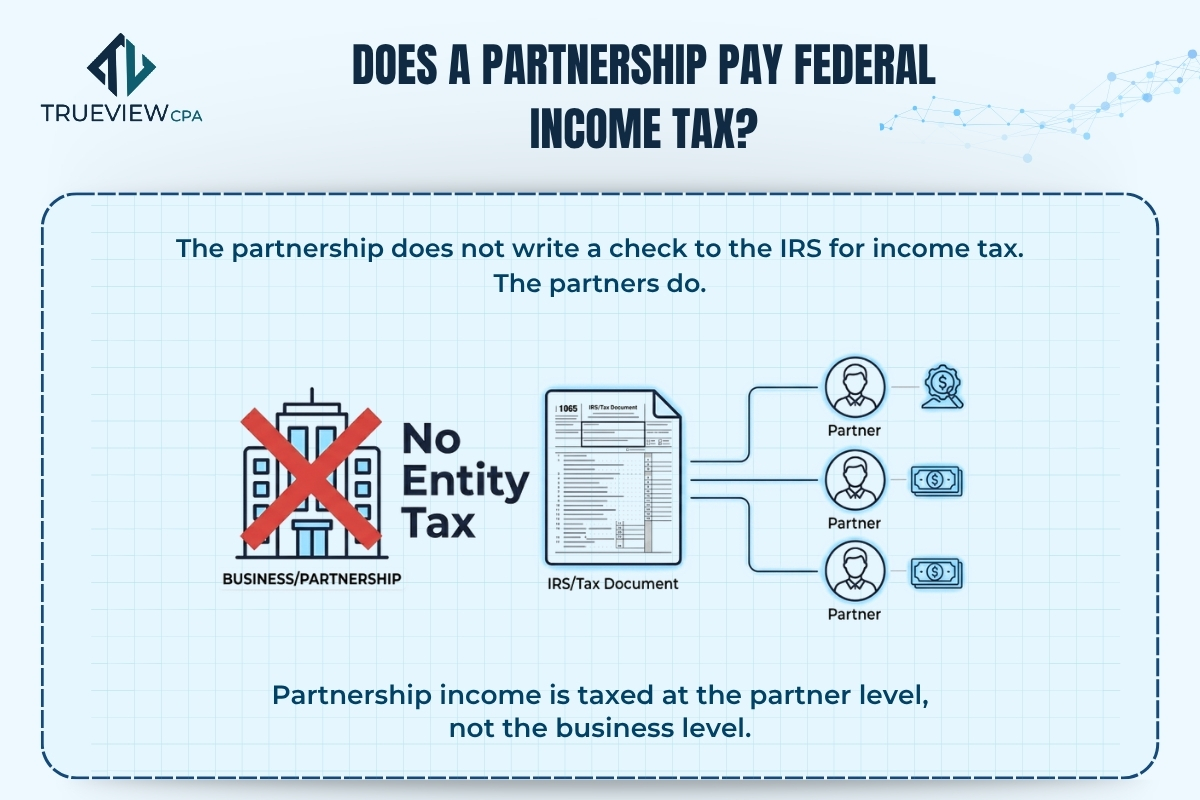

Under US federal tax law, a partnership is treated as a pass-through entity. This means the business itself is not subject to income tax. Instead, the profits, losses, deductions, and credits generated by the partnership flow directly through to each individual partner based on their ownership percentage or the terms of the partnership agreement. Each partner then reports their share on their own personal federal income tax return and pays tax at their individual rate.

The partnership does not write a check to the IRS for income tax. The partners do. This pass-through structure is one of the defining features of how the IRS treats partnerships, and it applies equally to general partnerships, limited partnerships, limited liability partnerships, and multi-member LLCs that have not made a tax classification election.

Even though a partnership does not pay federal income tax, it is still required to file a return with the IRS every year. That return is Form 1065, the US Return of Partnership Income. The 1065 tax return reports the partnership's total income, deductions, credits, and other financial activity for the tax year. It is an informational return, not a tax payment. No tax is remitted with the filing itself.

Attached to the 1065 is Schedule K, which summarizes the total amounts of each income and deduction category that need to be distributed across all partners. From Schedule K, the partnership prepares a separate Schedule K-1 for every partner. That K-1 is what each partner uses to complete their own individual return. If the 1065 partnership return is wrong, every K-1 that flows from it is wrong, and every personal return that relies on those K-1s is affected.

Each partner reports their distributive share of partnership income on their personal return and pays income tax on it at their individual rate. The important thing to understand is that this tax obligation is tied to the income being earned, not to whether any money was actually distributed.

If the partnership generated $300,000 in net income and your share is 40 percent, you report $120,000 on your personal return for the year, even if the partnership kept all of that money in the business and you never received a distribution. This catches a lot of new partners off guard in their first tax year.

Beyond income tax, general partners are also subject to self-employment tax on their distributive share of ordinary business income. For 2025, self-employment tax is 15.3 percent on net earnings up to the Social Security wage base and 2.9 percent on everything above that threshold. Limited partners are generally not subject to self-employment tax on their distributive shares, though guaranteed payments to any partner can still trigger it. Because no employer is withholding taxes from partnership distributions, partners are responsible for making quarterly estimated tax payments throughout the year.

A question that comes up often is whether these rules apply to an LLC. If your business is a multi-member LLC that has not elected to be taxed as a corporation, the answer is yes. The IRS treats a multi-member LLC as a partnership for federal tax purposes by default, which means it files Form 1065, prepares K-1s for each member, and follows all the same pass-through rules.

From a federal tax standpoint, a default multi-member LLC and a general partnership are treated almost identically. Both file a 1065 tax filing. Both issue K-1s. Both use pass-through taxation. The legal liability protection differs significantly between the two structures, but the federal tax mechanics do not. Many LLC owners discover this for the first time when tax season arrives, and if your multi-member LLC has not been filing a 1065 return, that is something worth addressing with a CPA sooner rather than later.

The 1065 filing deadline is March 15, one month before the individual return deadline of April 15. This earlier deadline exists so that partners have time to receive their K-1s and use them to complete their own returns. An automatic six-month extension is available by filing Form 7004, pushing the deadline to September 15. The extension applies to the filing only. If any entity-level tax is owed at the state level, that payment is still due by the original March 15 deadline.

Missing the deadline carries a penalty of $245 per partner per month for returns filed late, up to a maximum of 12 months. For a partnership with four partners filing three months late, that is nearly $3,000 in penalties before any other consequences are factored in.

Not every partnership tax return involves the same level of complexity. A two-person service business with straightforward income is a different return than a real estate limited partnership with depreciation, passive activity rules, and multiple investor classes. What every 1065 tax filing has in common, regardless of complexity, is that an error at the entity level cascades to every partner.

A misclassified deduction, an incorrect allocation, or a missed income item does not just affect one filer. It affects every K-1 that comes out of that return and every personal return built on top of it. 1065 tax preparation done by a CPA who works with partnerships regularly means the return is reviewed for accuracy before it goes out and every partner receives a K-1 they can rely on. 1065 filing services that include year-round support also make a meaningful difference when it comes to quarterly estimated payments, basis tracking, and planning for structural changes that could affect how income is taxed going forward.

At TrueView CPA, 1065 tax services for partnerships and multi-member LLCs are among our core areas of practice. If you have questions about whether your business needs to file a 1065 partnership return, or you want to make sure your partnership tax preparation is handled correctly this year, we are happy to start with a conversation.

Need help understanding partnership taxes and IRS filing requirements? Schedule a call with our tax experts today and get personalized guidance for your business.

.svg)